The Australian Prudential Regulation Authority (APRA) regulates credit unions and building societies as authorised deposit-taking institutions (ADIs).

In a recent speech Wayne Byres Chairman of APRA discussed the ability of mutual organisations such as credit unions and building societies to compete in the Australian banking system

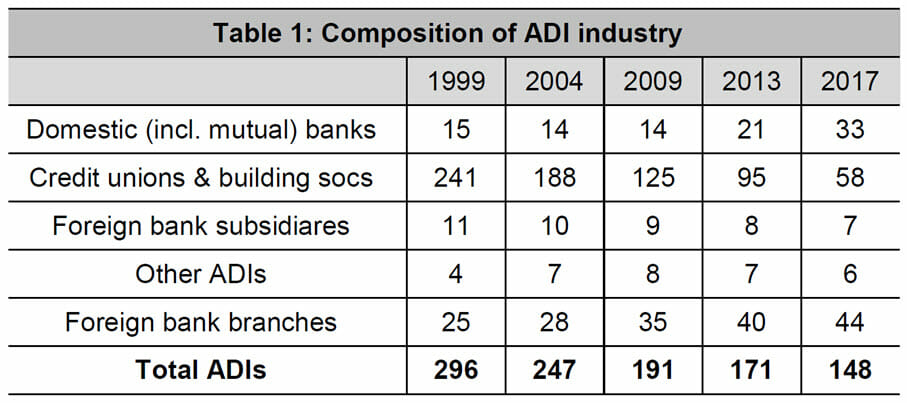

He observed that since 1999, the number of ADIs in Australia has halved nd that consolidation has occurred primarily in the mutual sector. By number, mutual ADIs made up four-fifths of the industry; that proportion is now just on half.

COBA Table 1: Composition of ADI Industry

Source: APRA

The increasing trend for credit unions and building societies (CUBS) to convert to mutual banks means that, by number, CUBS now account for under two fifths of ADIs. Given the Government’s proposed amendments to the Banking Act 1959 to allow all ADIs to brand themselves as banks, more CUBS will become mutual banks.

In terms of market share, mutual ADIs account for just over 2½ per cent of industry assets

Mr Byres pointed to a number of regulatory initiatives occurring that will help CUBS competitive position: capital requirements for mortgage lending relative to the largest banks have been adjusted, a new type of capital instrument will soon be available for mutuals, and APRA is exploring the potential for a simpler and low cost set of requirements for the smallest ADIs.

But the greatest impact on the business of banking will be the major technological changes at present. He concluded that “The digital revolution will challenge small ADIs’ ability to stay close to the forefront in retail product offerings, as well as bring new competitors with lower-cost business models.”